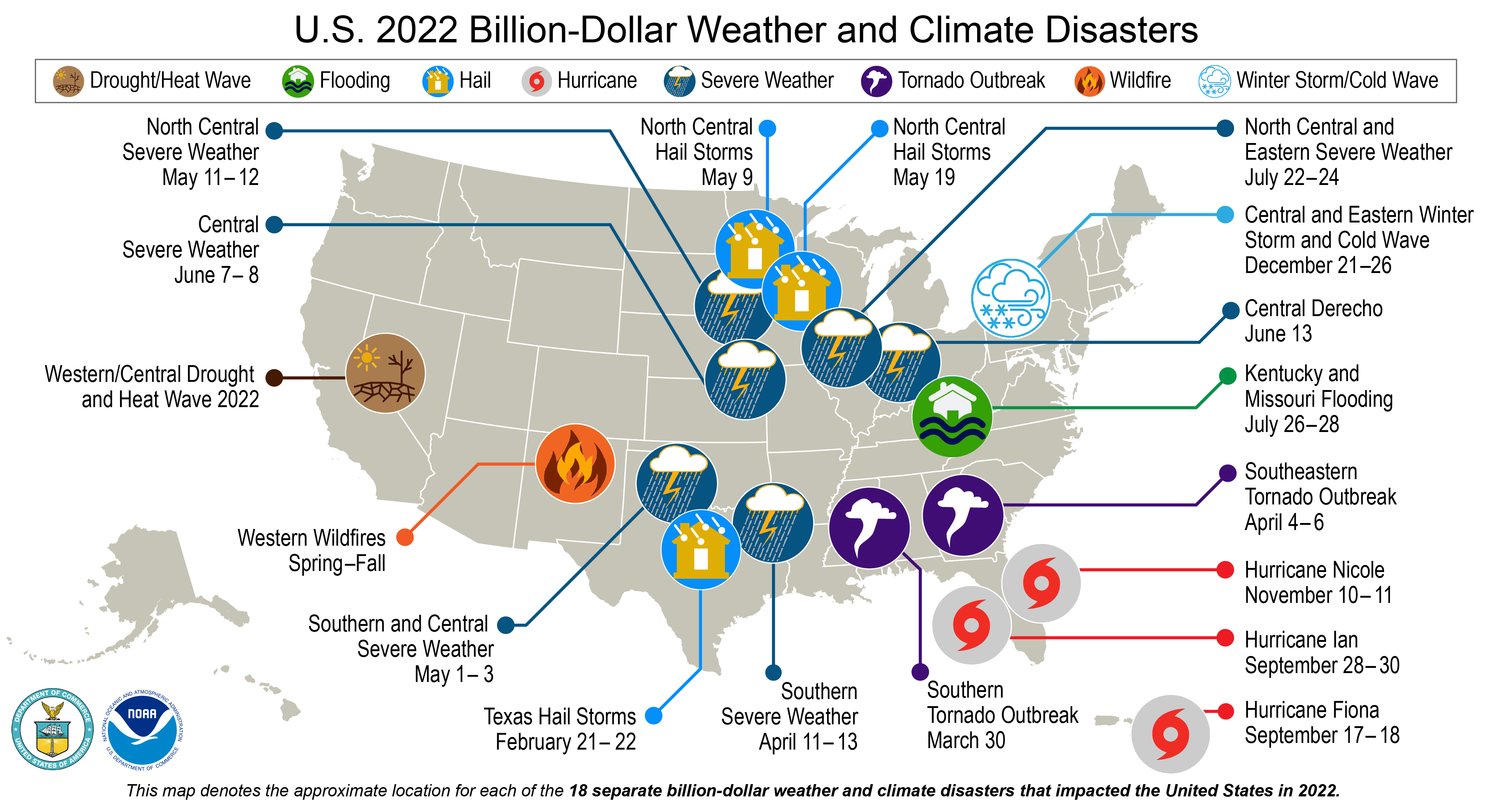

Issue: Natural disasters have an immense impact on the U.S. and global economy. According to a Swiss Re report, 285 natural catastrophe events occurred in 2022, causing the global economy $284 billion, down from $303 billion in 2021 but still well above the 10-year average of $220 billion. The insured portion was $125 billion in 2022, up from $121 billion in 2021 and above the 10-year average of $81 billion. According to the National Oceanic and Atmospheric Administration (NOAA), in 2022 there were 18 weather/climate disaster events in the United States with losses exceeding $1 billion each.

{kind=link}

Background: The growing frequency and severity of natural catastrophes warrant greater focus on natural catastrophe risk and resiliency. Maintaining healthy insurance markets through high loss years can be challenging as insurers must charge enough premium to maintain solvency while keeping insurance affordable for consumers. For this reason, the NAIC established a Climate and Resiliency Task Force in 2020 to serve as the coordinating NAIC body for discussion and engagement on climate-related risk and resiliency issues, including dialogue among state insurance regulators, industry, and other stakeholders. The Task Force established multiple workstreams to carry out its charges. The Climate Risk Disclosure Workstream revised the NAIC Climate Risk Disclosure Survey in 2022 to align the questions to the Financial Stability Board's Task Force on Climate-Related Financial Disclosure.

The survey is voluntary for states and territories to use at their discretion. All insurers licensed in a participating state/territory that reported in the prior year annual financial statement with at least $100 million in direct written premium across all lines of business countrywide must complete a survey. The survey is facilitated and administered by the California Department of Insurance (DOI), on behalf of all participating states. The California Department of Insurance maintains all insurer responses on the Climate Risk Disclosure Survey webpage. In November 2020, the Center for Insurance Policy and Research analyzed the data submitted by insurers and presented the findings in a report Assessment of and Insights from NAIC Climate Risk Disclosure Data.

The Pre-Disaster Mitigation Workstream developed a webpage to assist regulators in identifying ways to get involved in mitigating property loss and advocating for resiliency measures at the federal, state and local levels.

Status: NAIC members have taken an active role in educating Congress and providing feedback on various proposals regarding natural catastrophes. NAIC members have met with members of Congress and testified on important climate-related issues, stressing the role of the states in effectively managing insurance markets. In 2021, the NAIC outlined key ways state insurance regulators manage climate-related risks and respond to natural catastrophes in a report, Adaptable to Emerging Risks.

In 2020, 2021 and 2022 the NAIC Insurance Summit included a Natural Catastrophe Risk and Resiliency track. Content from those events can be viewed on the NAIC Library Archives.

2016

Regulators Respond to Disasters – NAIC Fall National Meeting 2016

This video shows disasters and response to wildfires in Tennessee, a tornado in Alabama and earthquakes in Oklahoma. It features then-NAIC President-Elect and then-Tennessee Insurance Commissioner Julie Mix McPeak.

Watch Video

2015

Regulators Respond to Disasters – NAIC Fall National Meeting 2015

NAIC members representing California, South Carolina, Texas and Washington discuss devastating floods and fires in 2015.

Watch Video

2013

Regulators Respond to Disasters in Arizona and Oklahoma

Then-Arizona Insurance Director Germaine Marks and then-Oklahoma Insurance Commissioner John Doak discuss disasters affecting insurance consumers in their states and the response coordinated by their departments, fellow regulators and the NAIC.

Watch Video

2012

Regulators Respond to Superstorm Sandy

Members of the NAIC discuss the impact of Superstorm Sandy in 2012. They describe efforts of state insurance regulators to address the needs of insurance consumers and the market in the wake of historic losses.

Watch Video

2011

Regulators Respond to Disasters

Members of the NAIC discuss the impacts of natural disasters in their states during 2011. They describe efforts of state insurance regulators to address the needs of insurance consumers and the market in the wake of historic losses.

Watch Video

Committees Related to This Topic

Additional Resources

NAIC Research Library Resources on Climate, Catastrophe, and Resilience

Assessments of and Insights from NAIC Climate Risk Disclosure Data (CIPR report, November 2020)

Assessing NAIC Climate Risk Disclosure Data (CIPR presentation, Sept. 10, 2020)

Task Force on Climate-Related Financial Disclosures

June 2019 Report

Translating Resilience Research (December 2019, NAIC Winter National Meeting presentation)

State and Local Policy Instruments for the Promotion of Catastrophe Mitigation

2017, Journal of Insurance Regulation

Natural Catastrophes, Insurance and Alternative Risk Transfer

November 2017, CIPR Newsletter

Catastrophe Risk and the Regulation of Property Insurance Markets

2016, Journal of Insurance Regulation

CIPR Symposium: Implications for Increasing Catastrophe Volatility on Insurers and Consumers

October 2014

NAIC Education & Training: Climate Change and Risk-Focused Examinations

Property and Casualty Insurance (C) Committee Public Hearing on Catastrophe Issues

December 2012

Guiding Principles for Consideration of Federal Catastrophe Insurance

CIPR Topic: Flood Insurance/National Flood Insurance Program (NFIP)

The Impact of Hurricane Sandy on the Financial Markets

NAIC Capital Markets Special Report (Nov. 16, 2012)

Presentations

- U.S./Global Natural Catastrophe Update

- Emerging Risks: Climate Change

- Emerging Risks: Climate Extremes in the U.S.

- Post Catastrophe Insurer Insolvencies

News Releases

NAIC Levels Up on Climate & Resiliency (July 7, 2020)

Changing Weather Patterns Mean Homeowners Need to Rethink Insurance Risks

March 29, 2017

NAIC Provides Support to Puerto Rico After Hurricanes

Sept. 29, 2017

NAIC Provides Support to US Virgin Islands After Hurricanes

Oct. 11, 2017

NAIC Leads Catastrophe Discussion

Feb. 27, 2014

Regulators Attend Post-Tornado Forum in Oklahoma

June 13, 2013

Testimony and Speeches

Managing Extremes in 2014 Forum

(Feb. 27, 2014 – Sen. Ben Nelson)

Contacts

Media queries should be directed to the NAIC Communications Division at 816-783-8909 or news@naic.org.

CIPR Staff

CIPRNews@naic.org